The Path to the Holy Grail: Solving the Stablecoin Trilemma

This article takes a deep dive into the significant attempts in the history of cryptocurrency to solve the Stablecoin Trilemma. By analyzing these efforts, the core of the problem is gradually uncovered, ultimately leading to an innovative solution.

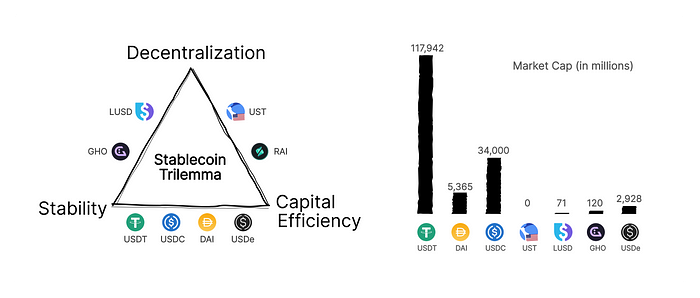

The Stablecoin Trilemma

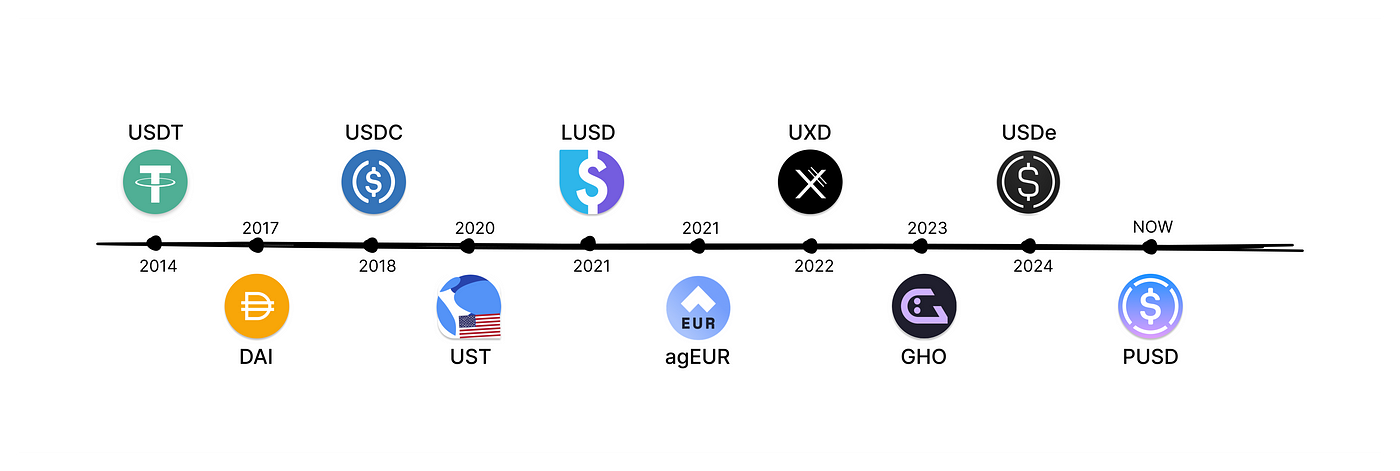

Currently, stablecoins with large market capitalizations are either fiat-backed stablecoins like USDT ($117 billion) and USDC ($35 billion), or hybrid stablecoins backed by both fiat and crypto assets like DAI ($5.3 billion). Purely crypto-collateralized stablecoins, such as GHO or LUSD, are much smaller in scale, around $100 million.

As for the once-prominent algorithmic stablecoins like LUNA’s UST, despite reaching a peak supply of $20 billion in 2022, they could not escape the fate of collapse. This article will not discuss this type of under-collateralized stablecoins in depth, as they cannot guarantee 100% redemption. Once confidence collapses, they fall into a death spiral, failing to achieve the most fundamental goal of stability as a stablecoin.

The Stablecoin Trilemma refers to the challenge of achieving stability, capital efficiency, and decentralization simultaneously. The pursuit of solutions to this trilemma has been a focal point in both academic research and practical applications. MakerDAO, with its decentralized stablecoin DAI, initiated the first large-scale implementation using Collateralized Debt Positions (CDPs). After the market disruption on March 12, 2020[1], MakerDAO introduced centralized stablecoins as collateral and then gradually increased its holdings of centralized assets, including U.S. Treasury bonds. Thus, DAI evolved into a hybrid stablecoin backed by both crypto and fiat assets.

The primary reason MakerDAO gradually shifted towards centralization is the inherent limitations of CDPs, specifically their high collateralization ratios and low capital efficiency. The current representatives of decentralized stablecoins still backed by CDPs, like Aave (GHO) and Liquity (LUSD), suffer from low capital efficiency, resulting in relatively small scales.

Delta-neutral Hedging Model

To address the low capital efficiency of the CDPs, some have turned to an alternative promising approach: the delta-neutral hedging model. For example, holding ETH spot and simultaneously taking an equivalent short position in ETH perpetual contracts can achieve perfect hedging, thereby insulating the underlying assets from ETH price volatility. The biggest advantage of this model is that it can achieve the same capital efficiency as fiat-backed stablecoins, where $1 of stablecoins is backed by $1 of underlying assets.

UXD was one of the early experiments in this direction[2], which relied on Solana’s decentralized perpetuals, Mango Markets, for hedging. However, the limited open interest (OI) of this exchange, combined with the risk of negative funding rates, severely limits the scale of UXD. Furthermore, Mango Markets suffered a $100 million loss in a 2022 hack, which dealt an additional blow to UXD. Following this, UXD couldn’t find a suitable hedging exchange and opted to hold USDC directly. UXD’s exploration of delta-neutral stablecoins ultimately ended in failure.

Angle Protocol adopted a different approach to the delta-neutral hedging model by issuing the euro-pegged stablecoin, agEUR. Unlike UXD, Angle integrated its own perpetual contract product called Hedging Agents. However, Angle’s perpetual contract product was not aligned with mainstream market demands, which prevented the protocol from scaling its hedging operations and led to the eventual abandonment of this strategy.

In 2023, Bitmex founder Arthur Hayes published an article, Dust on Crust[3], proposing a Delta-neutral model stablecoin that hedges through centralized exchanges, which led to the creation of Ethena. Ethena issued the stablecoin USDe through hedging on centralized exchanges and quickly achieved over $3 billion in supply by offering airdrop incentives and high APYs. While Ethena has successfully demonstrated the large-scale application of the delta-neutral model, it doesn’t represent an attempt to solve the Stablecoin Trilemma. Ethena not only holds centralized stablecoins like USDT but also introduces layers of risk associated with its own operations and those of third-party centralized exchanges. As Arthur Hayes mentioned, while it is true that Ethena’s USDe successfully breaks free from reliance on the banking system, it introduces various other centralized risks — raising the question: is this truly safer than relying on banks?

Vitalik’s Assertion

Following LUNA’s collapse, Ethereum’s founder Vitalik Buterin published an article titled Two Thought Experiments to Evaluate Automated Stablecoins[4], where he made an important assertion: “For a collateralized automated stablecoin* to be sustainable, it has to somehow contain the possibility of implementing a negative interest rate.” This statement was recently mentioned again in his comments on LUSD[5]. This is indeed a crucial issue.

If this assertion holds true, the conclusion Vitalik presented in the article is as follows:

Negative interest rates can be done in two ways:

1. RAI-style, having a floating target that can drop over time if the redemption rate is negative

2. Actually having balances decrease over time

Option (1) has the user-experience flaw that the stablecoin no longer cleanly tracks “1 USD”. Option (2) has the developer-experience flaw that developers aren’t used to dealing with assets where receiving N coins does not unconditionally mean that you can later send N coins. But choosing one of the two seems unavoidable — unless you go the MakerDAO route of being a hybrid stablecoin that uses both pure cryptoassets and centralized assets like USDC as collateral.

When a stablecoin’s price begins to fluctuate, or the quantity of stablecoins held by users changes automatically, it is difficult to imagine such a stablecoin gaining widespread adoption. Projects that have adopted either of these strategies have consistently failed to achieve significant progress, particularly those following Option (2), which tend to have a very short lifecycle. These stablecoins lack true competitiveness.

*Put simply, ‘automated stablecoins’ can be understood as truly decentralized stablecoins, since truly decentralized stablecoins must inherently operate without human intervention.

Negative Interest Rate

It is strongly recommended to read Vitalik’s original article, where he employs interesting thought experiments to explain why implementing negative interest rates is essential for automated stablecoins. Here, let’s revisit the importance of negative interest rates from the perspective of the delta-neutral model.

Let’s consider a delta-neutral stablecoin called dnUSD, backed by ETH and corresponding short positions. Clearly, an equivalent demand for long positions is necessary to facilitate the opening of short positions. Suppose a certain amount of dnUSD has been issued, and some users have taken corresponding long positions, bringing the system into balance. The potential future changes of the system can be simplified into four typical scenarios for analysis:

- The demand for dnUSD continues to increase, while the demand for long positions remains unchanged. This situation can be addressed by imposing a limit on new minting of stablecoins.

- The demand for dnUSD remains unchanged, but the demand for long positions increases. This can similarly be addressed by restricting users from opening new long positions.

- The demand for stablecoins decreases, but the demand for long positions remains unchanged. This scenario is manageable because the intrinsic value of the stablecoin remains stable, with both spot collateral and short positions intact. Restricting the closure of short positions will not result in losses for stablecoin holders, and users wishing to exit can sell in the spot market.

- The demand for stablecoins remains unchanged, but the demand for long positions decreases. This presents a challenge, as the previously simple methods may no longer be effective — restricting long users from closing positions is not feasible. Therefore, it becomes necessary to find a way to reduce the dnUSD supply accordingly. However, since the demand for stablecoins remains unchanged in this scenario, dnUSD holders lack the incentive to execute redemption or burning actions unless a form of negative interest rate is introduced.

It seems that negative interest rates are indeed unavoidable. But why hasn’t Ethena implemented them, yet still achieved large-scale supply without any issues? The answer is simple: Ethena is not one of the automated stablecoins Vitalik referred to. Centralized stablecoins enjoy more flexibility: when the demand for long positions decreases, they can simply close short positions and directly hold USDT.

Excess Demand Model

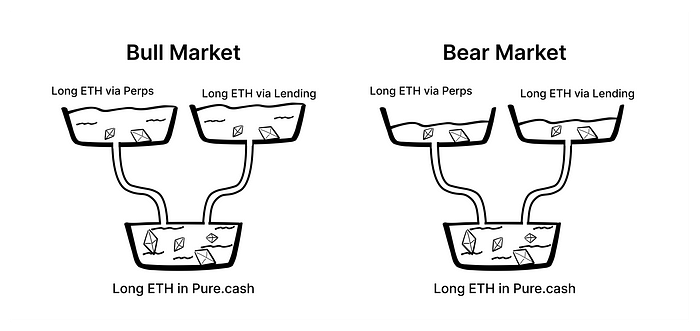

Is there no other solution? Let’s revisit the fourth scenario from the previous section, where stablecoin demand remains unchanged, but the demand for long positions decreases. Now, imagine a perfect perpetual contract product where the demand for long positions always exceeds supply and never diminishes — this would solve the problem, wouldn’t it? This concept forms the foundation of Pure.cash’s Excess Demand Model.

While it’s easy to make bold assumptions, the reality is that no perfect product exists, and some degree of compromise is inevitable. In the following section, we will gradually unveil the core mechanism of Pure.cash.

Creating sustained excess demand requires more than just offering a highly competitive product; it also necessitates ensuring that demand consistently exceeds supply. Pure.cash’s built-in LongOnly perpetual allows users to hold long ETH positions at zero cost by eliminating funding fees and charging only a market-average trading fee of 0.07%. Let’s explore the potential outcomes when such a product is widely adopted under two scenarios.

Currently, there are two mainstream methods to leverage long on ETH:

1. Through futures contracts, primarily perpetual contracts. The overall market for perpetual contracts is approximately $10 billion. Historical data shows that funding rates for perpetual contracts are typically positive for most of the year. Over the past year, Binance ETH long positions paid an average annualized interest rate of over 11%.

Although funding rates on these platforms often turn negative during bear markets, these periods are usually short-lived and highly volatile. Therefore, whether in a bull market with soaring funding rates or a bear market where rates turn negative, zero-cost long positions remain the optimal choice for most traders. This is because the duration of negative funding rates is unpredictable and could turn positive at any time, making them unfavorable for medium- and long-term positions.

2. Through lending: While precise data on market size is unavailable, estimates place it around $1–2 billion. Users collateralize ETH, borrow stablecoins, and purchase ETH in the spot market to achieve leveraged long positions. The lending market is relatively straightforward, with average stablecoin borrowing rates around 9%. Even if lending demand is insufficient and interest rates drop, they will not fall below zero. In this context, Pure.cash’s zero-cost long positions would undoubtedly be the optimal choice.

Additionally, zero-cost long positions are also an ideal hedging tool for arbitrageurs, significantly reducing their hedging costs or greatly improving capital efficiency. For instance, those engaging in cash-and-carry arbitrage in other futures markets can hold zero-cost long positions instead of spot assets. This enhances capital efficiency without incurring additional costs, thereby substantially amplifying their returns.

In summary, offering leverage for free in a market where leveraging typically incurs costs naturally creates a highly competitive product. However, the availability of such a product is inherently limited by the stablecoin supply. By further restricting this supply to remain below the lower bound of market demand fluctuations for long positions, it is possible to create a product that approaches an ideal state.

The Mechanisms of Pure.cash

Pure.cash also employs the delta-neutral hedging model, which effectively achieves both stability and capital efficiency. The remaining challenge lies in how to achieve decentralization — a topic we’ll now explore step by step.

It’s important to acknowledge that the decentralization of Pure.cash wouldn’t be possible without the pioneering efforts and contributions of earlier projects, most notably:

1. The perpetual contract AMM model created by GMX (later widely adopted by projects like Jupiter) laid the theoretical groundwork for Pure.cash’s LongOnly perpetual contract AMM model.

2. The Peg Stability Module (PSM) introduced by MakerDAO[6], which Pure.cash incorporates as a safeguard mechanism to be used only in extreme circumstances.

Building on these foundational innovations, Pure.cash offers a suite of products designed to tackle the stablecoin trilemma while introducing a highly competitive perpetual contract product and a highly lucrative yield-bearing asset. These include:

Pure USD (PUSD): A scalable, fully decentralized stablecoin.

LongOnly: An inverse perpetual contract product with zero funding fees.

Pure.cash Liquidity Provider Token (PLP): Provides liquidity for LongOnly and PUSD within its liquidity range and receives 35% of the trading fee income.

Based on the Excess Demand Model, the protocol limits the scale of long positions to maintain a state where long demand consistently exceeds supply. This corresponds to a 90% utilization rate of the PLP pool, which is considered optimal. This makes PLP an excellent yield-bearing asset, combining extremely low underlying volatility (ideally 10% of Ethereum’s volatility) with high yield driven by the continuous injection of 35% of trading fees.

It’s crucial to explain how the 35% trading fee income contributes to the ‘high yield’ of PLP. Since PLP only covers the difference between long positions (LongOnly) and short positions (PUSD), rather than the entire long positions, it achieves significantly higher capital efficiency. This efficiency is expected to be over three times that of GMX’s GLP, making PLP a highly lucrative asset.

Safeguard in Extreme Situations

Now it’s time to address the “inevitable compromise” mentioned earlier. The market environment is complex and unpredictable; even if we manage to maintain excess demand for long positions as discussed, black swan events remain unavoidable. A sudden market crash could cause long demand to rapidly decline beyond the buffer capacity of PLP. If short positions cannot be reduced accordingly, the protocol may be forced to hold volatile assets, compromising the delta-neutral objective of the stablecoin. However, to ensure a positive user experience for stablecoin holders, we have opted not to implement ‘negative interest rates,’ making it necessary to introduce alternative solutions to address this issue.

Pure.cash addresses this problem by introducing the Stability Fund and Active Redemption Mechanism. When the decline in long demand exceeds a certain threshold, the Stability Fund will buy back PUSD from the market and burn it, thereby synchronously reducing short positions to a safe level. If the buyback action causes the PUSD price to rise above its peg, the Stability Fund will buy USDC instead, mint PUSD 1:1 with USDC via the PSM (the stablecoins supported by the PSM can be adjusted by the DAO), then burn it and close the corresponding short positions.

Once the demand for long positions recovers or the supply of PUSD decreases (in this scenario, the protocol only allows burning and prohibits minting new PUSD, which further reduces the PUSD supply), the Stability Fund will reverse the process described above: minting PUSD through the protocol, exchanging it 1:1 with USDC via the PSM, and selling the USDC on the market.

Essentially, the PSM acts as a safeguard for system stability during extreme situations. As balance gradually returns, reliance on the PSM will be reduced to zero. In other words, for the majority of the time, Pure.cash will hold only native crypto assets like ETH. In extreme situations, Pure.cash may temporarily hold USDC as a reserve asset for PUSD. Once balance is restored, the USDC held will be automatically converted back to ETH. This approach not only addresses the potential risk of PUSD de-pegging upwards but also preserves the decentralization of the reserve assets.

Scalability of PUSD

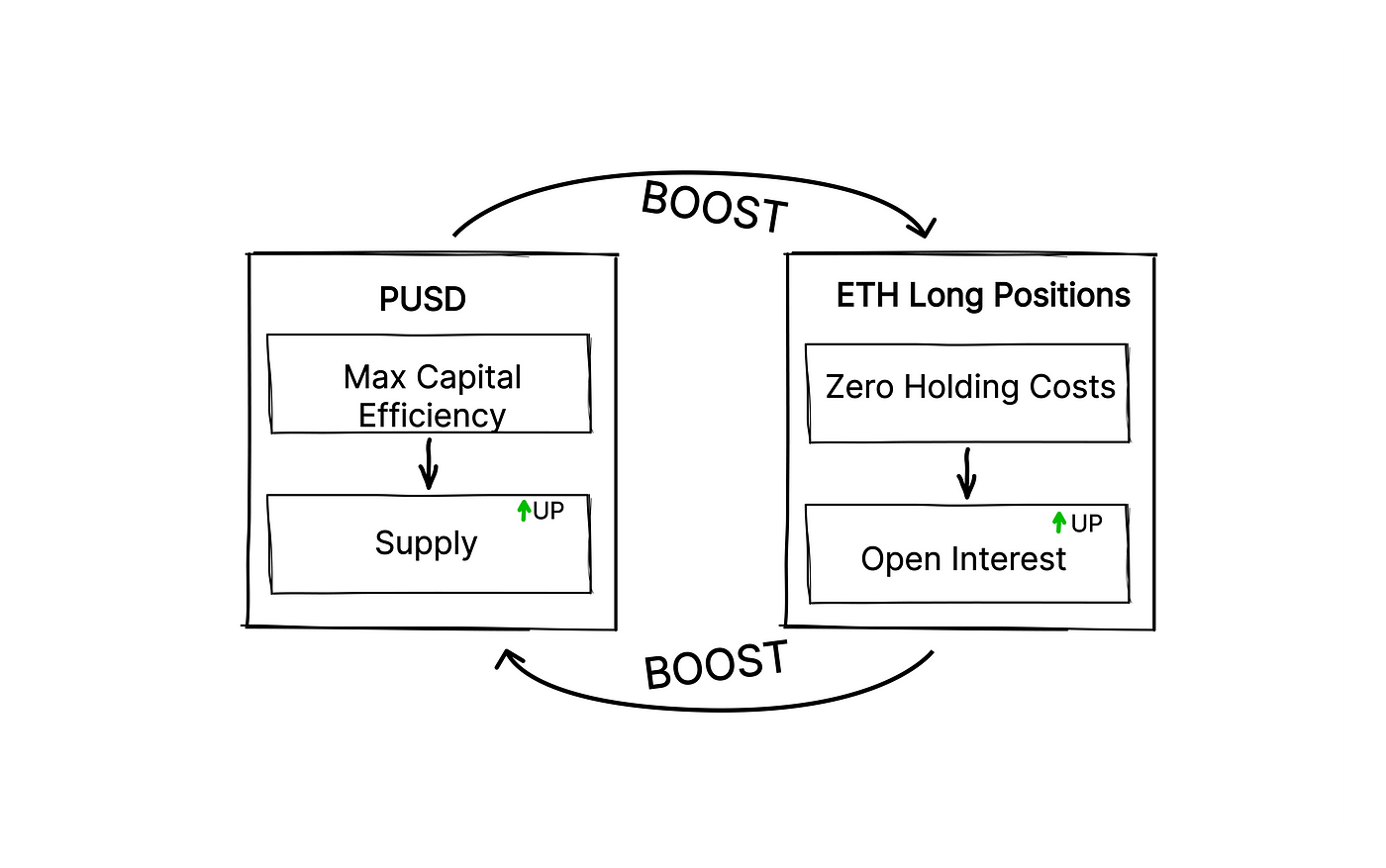

In its initial phase, Pure.cash has chosen to deploy on Ethereum and selected ETH as the underlying asset, as it is the only option that meets both fundamental requirements: the ability to deploy smart contracts and a sufficiently large market capitalization. Currently, ETH’s market cap is around $300 billion, with the perpetual contract market size at approximately $10 billion. Considering the further boost to long demand driven by zero-interest long positions, and the potential future growth of ETH’s market cap, we estimate that relying solely on ETH can support a PUSD supply of $3–5 billion currently, with the potential to expand to over $10 billion in the future.

Furthermore, since the issuance of PUSD is backed by an equivalent value of ETH, the larger the supply of PUSD, the greater the demand for ETH. This, in turn, will drive up the price and market cap of ETH. As ETH’s market cap increases, the potential for issuing more PUSD also grows, creating another positive feedback loop that mutually reinforces both assets.

References

[1] Tom Schmidt (2020), https://medium.com/dragonfly-research/daos-ex-machina-an-in-depth-timeline-of-makers-recent-crisis-66d2ae39dd65

[2] TUSHAR JAIN (2021), https://multicoin.capital/2021/09/02/solving-the-stablecoin-trilemma/

[3] Arthur Hayes (2023), https://blog.bitmex.com/dust-on-crust/

[4] Vitalik Buterin (2022), https://vitalik.eth.limo/general/2022/05/25/stable.html

[5] Vitalik Buterin (2024), https://warpcast.com/vitalik.eth/0x28cb7919

[6] MakerDAO (2020), https://mips.makerdao.com/mips/details/MIP29

Disclaimer

In line with the Trust Project guidelines, please note that the information provided on this page is not intended to be and should not be interpreted as legal, tax, investment, financial, or any other form of advice. It is important to only invest what you can afford to lose and to seek independent financial advice if you have any doubts. For further information, we suggest referring to the terms and conditions as well as the help and support pages provided by the issuer or advertiser. MetaversePost is committed to accurate, unbiased reporting, but market conditions are subject to change without notice.

About The Author

Gregory, a digital nomad hailing from Poland, is not only a financial analyst but also a valuable contributor to various online magazines. With a wealth of experience in the financial industry, his insights and expertise have earned him recognition in numerous publications. Utilising his spare time effectively, Gregory is currently dedicated to writing a book about cryptocurrency and blockchain.

More articles

Gregory, a digital nomad hailing from Poland, is not only a financial analyst but also a valuable contributor to various online magazines. With a wealth of experience in the financial industry, his insights and expertise have earned him recognition in numerous publications. Utilising his spare time effectively, Gregory is currently dedicated to writing a book about cryptocurrency and blockchain.